What Will The MSCI Frontier Markets 100 Index Look Like Without Kuwait?

Kuwait will spend its final day classified as a Frontier Market on November 30th 2020 as Morgan Stanley Capital International (MSCI) prepares to upgrade the Middle Eastern nation to the Emerging Markets category. While investors look to capitalise on the move by investing in Kuwait-focused equities (such as the Invesco Kuwait ETF and iShares Kuwait ETF), we ask the question: what will the MSCI Frontier Markets 100 Index look like without Kuwait?

The Process

Before diving into the numbers, it is important to note that MSCI is planning on phasing-out Kuwaiti equities from the MSCI Frontier Markets 100 Index in five tranches across five successive Index Reviews, starting from the November 2020 Semi-Annual Index Review (SAIR) and ending in the November 2021 SAIR in a bid to alleviate any potential implementation concerns for the Index. This will not effect Kuwait’s upgrade from the MSCI Frontier Markets Index to the MSCI Emerging Markets Index, which will take place in one step as of the close of Monday 30th November 2020 (effective Tuesday 1st December 2020). The implementation was originally expected to commence in May 2020, but was delayed because of the global COVID-19 pandemic.

Kuwaiti equities will be added to the MSCI Emerging Markets Index at an aggregate weight of 0.58% at the end of the process. This means it will have a larger position than the likes of Peru, Argentina and Egypt in the EM Index.

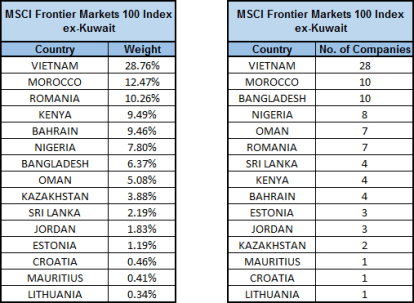

MSCI Frontier Markets 100 Index ex-Kuwait

MSCI Frontier Markets 100 Index ex-Kuwait: country weightings and count of constituents

Once Kuwait leaves the MSCI Frontier Markets 100 Index, Vietnam will become the largest constituent and will enjoy a 28.76% shares in the Index, more than double its current position (approximately 13.12%). Vietnam’s position as a Frontier Market has been a hot topic for many investors and analysts, with many believing that it should be promoted to an Emerging Market in the near future. The Asian nation narrowly missed out on a promotion to the FTSE Emerging Markets Index earlier this year, but there are positive signs as officials in the country have announced various initiatives to boost its chances of a promotion from MSCI, FTSE and S&P. Becoming the largest constituent in the Index may also provide a significant boost to their upgrade ambitions.

Morocco (12.47%) and Romania (10.26%) will be the second and third largest constituents respectively in the Index post-Kuwait, with the latter enjoying a relatively significant boost from its current weight of 7.9%. Kenya (9.49%) and Bahrain (9.46%) complete the Top 5. Croatia, Mauritius and Lithuania will all have allocations of less than 1% and will each have one stock in the MSCI Frontier Markets 100 Index (Valamar Riviera, Lighthouse Capital and Bank of Siaulio respectively).

In terms of number of stocks in the MSCI Frontier Markets 100 Index post-Kuwait, Vietnam will have the most with 28 companies being represented in the Index, followed by Morocco and Bangladesh who will both have 10. Nigeria (8), Oman (7) and Romania (7) also have a relatively significant amount of constituents. The five largest companies in the Index will be: Ahli United Bank (Bahrain, 7.47%), Safaricom (Kenya, 5.43%), Vietnam Dairy Products (Vietnam, 4.51%), Maroc Telecom (Morocco, 4.46%) and Vingroup (Vietnam, 4.42%).

On a sector level, it should be noted that Kuwaiti equities, which make up just over 25% of the MSCI Frontier Markets 100 Index pre-upgrade, are primarily stocks in the Financials sector. Therefore, the removal of the two largest Kuwaiti financial constituents – National Bank of Kuwait (c.10.75%) and Kuwait Finance House (c.4.62%) – as well as other smaller members, means that the concentration of stocks in Financials sector will significantly decrease, which currently comprise of just under half of the Index. This means that the new MSCI Frontier Markets 100 Index will become slightly more diverse once Kuwaiti equities have been phased out.

MSCI also confirmed that the weights of Bangladesh and Nigeria will remain unchanged in the MSCI Frontier Markets 100 Index as they, alongside Lebanon, are currently being closely monitored on liquidity and accessibility of their markets and have had a “Limited Investability Factor (LIF)” applied on their securities. Bangladesh is on the list due to the introduction of a floor price for all securities on the Dhaka Stock Exchange, while Nigeria’s plight lies in the deterioration of liquidity in the Nigerian FX market. Although no Lebanese stocks are represented in the MSCI Frontier Markets 100 Index, the country’s Frontier Market status is currently under threat and it may be downgraded to a “Standalone Market” in 2021.

Potential Changes

It is well worth remembering that the above will not be fixed and is subject to changes in economic, political and market positions for each country. Also, not only can member constituents change, but whole countries may enter or exit the MSCI Frontier Markets 100 Index during the transition period over the next 12 months. Aside from the potential changes mentioned earlier in the article (Vietnam promotion; Nigeria, Bangladesh and Lebanon demotion), the below three scenarios may also be worth looking out for:

Country 1: Argentina

Despite narrowly retaining its Emerging Market status earlier this year in June, Argentina may be reclassified to a Frontier Market if capital controls remain in place and market sentiment is further damaged. Argentina was upgraded from the MSCI Frontier Markets Index in May 2019, but its status is now under scrutiny from MSCI.

Country 2: Turkey

Turkey’s fate as an Emerging Market also hangs in the balance after MSCI warned that it may be downgraded to either Frontier Markets status or Standalone Market Status if accessibility levels in the Turkish market continue to deteriorate after officials in the country imposed bans on short selling and stock lending in October 2019 and February 2020 respectively. Turkey’s current position in the MSCI Emerging Markets Index is currently less than 0.5% (lower than Kuwait’s allocation).

Country 3: Iceland

On a more positive note, Iceland was promoted from a Standalone Market to a Frontier Market by MSCI in June 2020. MSCI launched a consultation last year regarding the representation of Icelandic stocks in the MSCI Frontier Markets 100 Index (ex-Kuwait) and there is a chance that eleven stocks will make up 9% of the Index, with Marel being the country’s largest allocation (3.6%). If included, Iceland will become a significant player in the Index.

Summary

Kuwait’s ascension to the Emerging Markets category will mean that other countries will have the opportunity to shine in its absence. Countries such as Vietnam, Morocco and Romania will now hold more prominent positions in the MSCI Frontier Markets 100 Index, thus becoming more likely to be considered themselves for the much-coveted promotion to the MSCI Emerging Markets Index. Meanwhile, the inclusion of Kuwait in its new Index may spell pressure for some of the small constituents, including the likes of Argentina, Turkey and Peru.

Leave a comment