Tough Road Ahead for India’s Global Debt Ambitions

The ongoing COVID-19 crisis has hurt India’s ambitions to attract global capital into its local debt markets, as the health pandemic continues to weigh on the country. Given this setback, we ask: “Can India’s local debt still go global?”. Economics Global takes a further look.

India’s global ambitions to attract foreign money and investors into its financial markets has hit a snag once again, after starting to make some recent progress after years of “all talk but no action.”

A surge in COVID-19 cases, a second cut in its sovereign credit rating this year, and recent tensions with China in the Ladakh region, has shoved India back into the global spotlight in recent weeks. Unfortunately, this all couldn’t come at a worse time for the country, especially at a time when Indian lawmakers have been working hard to open India’s financial markets to global investors and traders. Rather than celebrate fresh new capital coming into India’s bond markets, the country is grappling with an increasing list of internal and external issues.

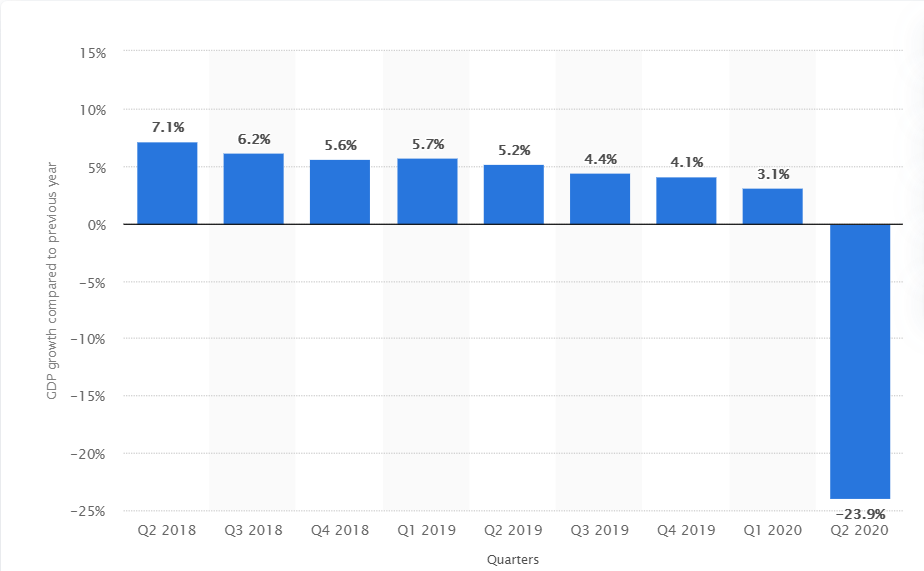

After years of rapid growth, making India one of the world’s fastest growing economies in recent years, the country’s economic fortunes seem to have hit a wall in 2020, as India grapples with surging COVID-19 cases in recent weeks. This has made India one of the top hot spots for the virus at the moment, alongside Brazil and the US.

As a result of the ongoing health crisis, India is currently undergoing its worst recession on record, with the unemployment rate rising to an historic 24%. On the fiscal front, the additional government spending is forecast to increase the budget deficit to 11%, pushing the country’s debt-to-GDP ratio past 80%. As a result, in June the ratings agency Moody’s issued a “Negative” outlook for the country, and cut its credit rating from “Baa2” to “Baa3” for Indian sovereign bonds.

The recent ratings cut to the country’s economic outlook, coupled with the internal and external geopolitical and health issues currently affecting the country, leaves Indian sovereign debt struggling to hang on to its investment grade status. As a result of these headwinds, India’s sovereign debt could be thrust into ‘junk’ status for the first time in over 14 years. In fact, investors don’t have to look far to see the market effects of the loss of “Investment Grade Status” on an Emerging Market, as countries such as Brazil and South Africa have shown the cost of losing the coveted investment classification in recent years.

India has been trying to open its financial sector to global investors, as well as internationalize the Indian Rupee for global trade and commerce for over a decade, but to little avail. Though India has had some success in attracting foreign investors into its equity markets, growing its equity market capitalization to over US$2.2 trillion as of 2019, its debt markets haven’t had as much success.

As of 2019, less than 4% of Indian sovereign bonds are held by foreign investors, compared to 20% to 40% in neighbouring countries like Malaysia and Indonesia. Further, corporate bond issuance by Indian firms was only 4% of Indian GDP – much lower than other major Emerging Markets.

Despite being a laggard in the global fixed income markets, in comparison to their Emerging Market and regional peers, India is taking steps to showcase its debt markets to attract foreign capital. In March, the Reserve Bank of India took its first real steps to address this, by turning away from the 6% limit on foreign ownership of Indian sovereign bonds, utilizing the Fully Accessible Route (FAR) plan to allow unlimited access for a select group of benchmarks. The removal of the 6% limit on foreign ownership of Indian government debt is a major step forward for Indian capital markets. Previous ownership limits on Indian government bonds have kept them out of major global bond indices, such as the Bloomberg Barclays Global Aggregate Index, forcing bond investors to look elsewhere for investment opportunity.

Given these changes to the FAR initiative, global investors and financial institutions have taken note of India’s changes, and have begun to give Indian debt a second look. In June, JPMorgan tagged India as one the four countries it is reviewing for inclusion in the JPMorgan Government Bond Index-Emerging Markets (GBI-EM) Indices, a move that did wonders for Chinese bonds in 2019. If included, Indian bonds could make up approximately 7.8% of the index.

However, there are still some obstacles in the country’s way before being included within the JPMorgan GBI-EM Index. Since only 9% of India’s government debt stock is covered by the FAR rules, this keeps Indian government bonds just shy from inclusion. Further, the index requires sovereign bonds to have an investment grade rating for inclusion within the index, as well as maintain that rating to avoid being removed. Additionally, the lack of the internationalization of the Indian Rupee does not help India’s case here either. There has been little progress in making the Rupee a global currency, as currently there is very little incentive for international firms to invoice in the currency, especially in comparison to India’s Emerging Market and regional counterparts. Though Masala bonds – Rupee-denominated bonds issued outside of India – have made their way into the international markets, demand for them is quite low.

Going forward, it will be interesting to see what (further) steps India will take to open up its debt markets, and rival that of its Emerging Market peers such as China, South Africa, and Brazil. To do so, we believe the most important step is for the country to find a way to make its fixed income markets more attractive to global investors and capital. Though reforms such as the FAR plan, and India’s possible inclusion into the GBI-EM index do bode well for the country, New Delhi’s reluctance to issue US dollar-denominated debt, as well as the risk of another ratings downgrade, indicates the country still has a long way to go.

Though India is taking concrete steps to internationalize its bond markets, it will be a tough and long road ahead for the country.

© 2020 Economics Global Inc.

Content Disclaimer

Any views expressed here are those of Economics Global Inc. as of the date of this publication, are based on available information, and are subject to change without notice. This document does not constitute investment advice.

The value of investments and the income they generate may go down as well as up and it is possible that investors will not recover their initial outlay. Past performance is no guarantee for future returns.

See Tomorrow Economy Today

Visit us at www.economicsglobal.com and join our mailing list for our updates on the trends shaping the global markets and the international economy.

Follow Us On Social Media

LinkedIn: https://www.linkedin.com/company/economics-global

Twitter:

Facebook:

https://www.facebook.com/EconomicsGlobal

Instagram:

Leave a comment