What Will MSCI’s Frontier Market Index Look Like Without Pakistan?

In light of Pakistan’s upcoming reclassification to “Emerging Market” status, Morgan Stanley Capital International (MSCI) has announced that it has launched a consultation on changes in the MSCI Frontier Markets 100 Index. But the big question remains: what will this index look like without Pakistan?

Simulated MSCI Frontier Markets 100 Index (“FM 100 Index”)

MSCI’s consultation will not only look at the changes in the composition of companies and countries in the index once Pakistan leaves, but will also propose to include new securities in the FM 100 Index outside of its Semi-Annual Index Reviews.

The removal of Pakistan from the FM 100 Index will lead to the number of securities needed to meet the index’s requirement to fall below the minimum of 85 constituents (from 90 to 77), meaning that 9 securities will need to be artificially maintained in order to exceed this amount. MSCI’s proposition is to lower the free float-adjusted market capitalisation cutoff to correspond to a cumulative coverage of 90% of the MSCI Frontier Markets Investable Market Index (up from 80%). MSCI also proposes increasing the total number of constituents to 107 (higher than its current level of 90).

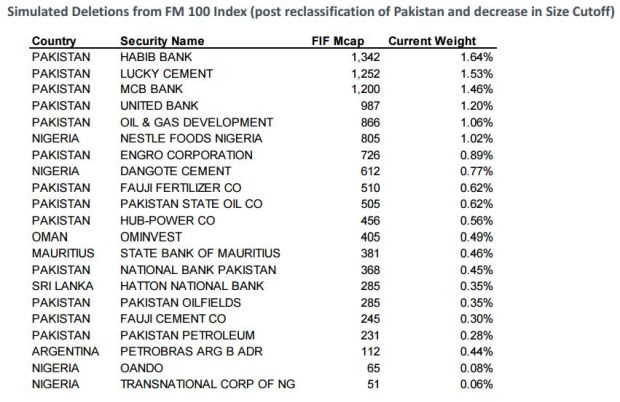

MSCI conducted simulations of the potential additions and deletions from the index, with the latter including companies from countries other than Pakistan. The largest addition is Vietnam Dairy Product, while notable non-Pakistani deletions include Nestle Foods Nigeria, Dangote Cement (Nigeria) and Oman’s Ominvest. Bangladesh will gain the most constituents, increasing its current number by 11, while Nigeria will lost 4 securities in the newly formed index.

Simulated Additions to the MSCI Frontier Markets 100 Index after Pakistan has been reclassified.

Simulated Deletions from the MSCI Frontier Markets 100 Index after Pakistan has been reclassified.

In terms of country and individual company weightings, the additions and deletions from the FM 100 Index yields interesting results:

Simulated MSCI Frontier Markets 100 Index after Pakistan has been reclassified (countries and constituents).

Firstly, Kuwait (21.3%), Argentina (18.7%) and Vietnam (11.6%) will enjoy the largest weightings in the index. This represents a slight decline for the first two compared to the Index at this present time (22.21% and 19.89% respectively) and an approximate 4% increase in weighting for Vietnam, primarily due to Vietnam Dairy Product’s addition to the Index and a recent addition of two new securities to its index. In total, these three countries represent 51.64% of the index in the simulation.

In terms of the number of securities per country in the index, Bangladesh tops the list with 17 (largest constituent being Square Pharmaceuticals with a 1.37% weighting), while Kuwait (15), Vietnam (14) and Argentina (14) closely follow. There are no countries with a solitary security in the simulated index, but the countries at the other end of the spectrum only have 2 securities: Slovenia, Sri Lanka, Bahrain and Mauritius.

Kuwaiti securities dominate the largest individual constituents in the simulated index, with the National Bank of Kuwait retaining the top spot with a weighting of 6.09%, slightly lower than its current weighting of 6.39%. Nigerian Breweries, which represents half of Nigeria’s stake in the Index, manages to increase its weighting and make it into the Top 10. The largest 10 constituents will represent 36.13% of the index, a very small decline from 36.34%.

Other Index Review Changes

MSCI has proposed to implement the upcoming May 2017 Index Review changes in the FM 100 Index over four consecutive months (May 2017 to August 2017) in order to maintain turnover at its usual historical levels and provide a buffer against the potential market impact. The phasing in would be done on a 40-20-20-20 basis, i.e: 40% of changes in May 2017, with small proportions of 20% being implemented at the end of June, July and August.

In order to determine the new weightings, MSCI will calculate the security index weights post-reclassification; calculate the difference between the current security index weights and the security index weights post-reclassification, then apply the following formulae:

i. Phase 1 (May 2017) => New Weight = Current Weight + (Weight Difference * 40%)

ii. Phase 2 (June 2017) => New Weight = Current Weight + (Weight Difference * 33%)

iii. Phase 3 (July 2017) => New Weight = Current Weight + (Weight Difference * 50%)

iv. Phase 4 (August 2017) => New Weight = Post-Reclassification Weight

Let’s take Bangladesh’s BRAC Bank as an example (a proposed new constituent). Its current weighting is 0% (as it’s new) and it has a post-reclassification weighting of 0.38%. In the first phase, its weighting will be 0.152%; second phase at 0.228%; third phase at 0.304%; before finally converging to its post-reclassification weight. The same logic can be applied to securities being deleted from the index, as well as weighting increases and decreases.

Alongside implementing changes over four successive months, MSCI is also proposing the likes of initial public offerings (IPOs) and spin-offs to be including in the FM 100 Index, provided that they have been included in the FM Investable Markets Index (FM IMI) and that the market cap exceed 1.8 times the Size Cutoff for the FM 100 Index.

Under this proposal, the likes to No Va Land Investment Group (Vietnam), Vietnam Dairy Product (Vinamilk) and Seplat Petroleum Development Company (Nigeria) would have been added to the FM 100 Index as soon as they were introduced to the FM IMI, rather than waiting for the semi-annual review to take place. This proposal may also work in Vietnam’s favour with many IPOs on the horizon, such as the eagerly anticipated and internationally marketed $170 million IPO of low-cost airline Vietjet, which has attracted the likes of BNP Paribas and JP Morgan.

MSCI will discuss all of the points above and will, hopefully, provide us with more concrete answers within the next few months. The document entitled “Consultation on Proposals for the MSCI Frontier Markets 100 Index” by MSCI can be found here.

By James Eugene

Leave a comment